10 Jan 2024

How to secure a competitive interest rate to cut your mortgage costs

With interest rates at their highest level since the 2008 financial crisis, finding a mortgage deal that’s right for you could save you thousands of pounds over the long term.

Following the 2008 financial crisis, the BoE slashed its base interest rate, and it remained below 1% for more than a decade. During the Covid-19 pandemic, it cut the rate to just 0.1%. This means the cost of borrowing was low and aimed to encourage households and businesses to spend more.

However, once inflation started to rise at the end of 2021, the BoE began to increase the base rate to curb spending. As of December 2023, the BoE base rate is 5.25%. For many mortgage holders, this has led to repayments rising.

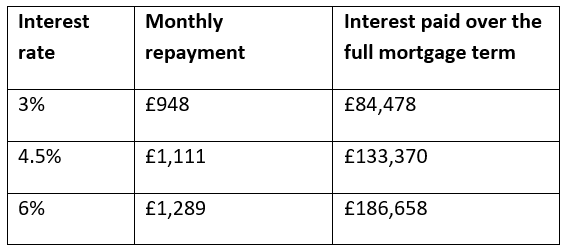

The table below shows how the interest rate you pay could affect your monthly repayments and the total cost of borrowing if you took out a £200,000 repayment mortgage with a 25-year term.

Source: MoneySavingExpert

It’s important to note that the interest rate you pay will usually change during the term of your mortgage. Typically, the rate you pay will fall as you build up more equity in your property and present less of a risk to lenders. However, the above example demonstrates the effect interest rates have on both your short- and long-term finances.

So, if you’re mortgage deal is expiring, what could you do to improve your chances of securing a competitive interest rate?

Step 1: Put yourself in a good position to approach lenders

Before you start applying for a new mortgage, reviewing your finances and credit report could be useful.

Lenders will assess your application to weigh up how much risk there is of you defaulting on your repayments. So, taking steps to put yourself in a good position before applying could be valuable.

Reviewing your credit report is often a good place to start, as lenders will use this when assessing your application – is the information in your report correct? Are there any potential red flags that could put lenders off? There might be small steps you could take that may improve how you appear to lenders, such as closing down old accounts.

You might also want to get your home revalued. If the value of your home has increased, the equity you hold could be higher than you expect. When making an offer, a lender will consider your loan-to-value (LTV) ratio, which compares how much you’d borrow against the value of the property.

Usually, the lower the LTV, the more competitive the interest rate you’ll be offered as you’ll be viewed as less of a risk.

Step 2: Search the mortgage market for a deal that’s right for you

There are lots of mortgage lenders to choose from, and some of them don’t have a high street presence. Interest rates offered by different lenders can vary significantly, so taking the time to search the market could help you find a deal that’s right for you.

Yet, searching the mortgage market can be a challenge.

As each lender will set their own criteria, it can be difficult to understand which lenders are most likely to accept your application. A rejected application could lead to delays, potentially cost you money, and may result in a hard credit check on your credit report, which could affect your application when applying to other lenders.

In addition, the mortgage market can change quickly. Indeed, according to Moneyfacts, the average shelf-life of a mortgage deal in November 2023 was just 20 days.

Working with a mortgage broker could be useful. As experts, we can take the time to understand your circumstances and search the market with these in mind to find a deal that suits you.

The interest rate isn’t the only factor you should review when assessing mortgage deals

When you’re weighing up your mortgage options, the interest rate is likely to be a key factor. However, depending on your circumstances, there might be other areas you want to consider too.

For instance, if you plan to move, could you port your mortgage to a new property? Or, if you’d like to reduce your debt quickly, could you make overpayments without facing a fee?

Thinking about what’s important to you and your long-term plans when you’re searching for a mortgage could help you secure a mortgage that’s right for you.

Contact us to discuss your mortgage

As a mortgage broker, we can offer guidance throughout the mortgage process and search the market on your behalf. Please contact us to arrange a meeting.

Please note:

This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

Your home may be repossessed if you do not keep up repayments on a mortgage or other loans secured on it.